| PURE CYCLE Exhibit 99.2 CORPORATION FINANCIAL RESULTS Q1 -2026 EARNINGS PRESENTATION - - Presented By: MARK HARDING WWW.PURECYCLEWATER.COM |

| PURE CYCLE CORPORATION PAGE 2 FORWARD LOOKING STATEMENT Statements that are not historical tacts contained or incorporated by reference in this presentation are "forward-looking statements" ("FLS"} within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21 C of the Securities Exchange Act of 1934 as amended. FLS involve risks and uncertainties that could cause actual results to differ from projected results. The words "anticipate," "believe,'' "estimate," "expect," "plan," "intend" and similar expressions, as they relate to us, are intended to identify FLS. Such statements reflect our current views with respect to future events and are subject to certain risks, uncertainties and assumptions. We are not able to predict all factors that may affect future results. We cannot assure you that any of our expectations will be realized. Our actual results could differ materially from those discussed in or implied by these forward-looking statements. Factors that may cause actual rnsults to dirffer materially from those contemplated by such FLS include, without limitation: the ri sk factors discussed in our most recent Annual Report on Form 10-K; the timingr of new home construction and other development in the areas where we may sell our water, which in turn may be impacted by credit availability; popt.Jllation growth; employment rates; greneraI1 economic conditions; the market price of water; changes in customer consumption patterns; changes in applicable statutory and regulatory requirements; changes in governmental policies and procedures; uncertainties in the estimation of water available under decrees; uncertainties in the estimation of costs of delivery of water and treatment of wastewater; uncertainties in the estimation of the servi'Ce life of our systems; uncertainties in the estimation of costs of construction projects; uncertainties in the amount and timingr of reimbursable public improvement payments: uncertainty in the single family home rental market and our ability to rent homes in a timely manner or at the amount we project; the strength and financial resources of our competitors; our ability to find and retain skilled personnel; climatic and weather conditions, including flood, droughts and freezing conditions; labor relations; availability and cost of labor, material and equipment; delays in anticipated permit and construction dates; environmental risks and regulations; our ability to raise capital; our ability to negotiate contracts with new customers; and uncertainties in water court rulings; and other factors discussed from time to time in our press releases, public statements and documents filed or furniished with the SEC. |

| MARK W. HARDING President, CEO, and Director Mark is an exceptional leader who has significantly shaped Pure Cycle's success. Under his 35-year tenure, the company has successfully acquired over $130 million in water and land interests. His vision and strategic acumen have been instrumental in the company's growth and impact. MARC SPEZIALY VP, CFO, Principal Accounting Officer, Principal Financial Officer Marc brings over 20 years of financial expertise. He manages our financial operations and single-family rentals. Marc obtained his bachelor's degree in Accounting and Finance from the University of San Francisco and is a licensed Certified Public Accountant. RACHELLE BEAUDRY Head of Marketing BRENT BROUILLARD Vice President, Engineering Brent Brouillard, Vice President of Engineering at Pure Cycle since 2017, oversees the planning, design, and operation of water and wastewater systems in the Denver-Metro area. A licensed Professional Engineer with fifteen years’ experience, he holds degrees in Civil Engineering and Hydrology from the University of Wyoming and Colorado School of Mines. DIRK LASHNITS Vice President, Land Development Dirk is a seasoned leader with a Civil Engineering background and over two decades of local land development experience. He skillfully guides land development, entitlements, and construction, playing a vital role in advancing corporate objectives, risk management, and project success. PURE CYCLE CORPORATION PAGE 3 |

| PURE CYCLE CORPORATION PAGE 4 BOARD OF DIRECTORS Mark W. Harding Patrick J. Beirne Susan D. Heitmann Wanda J. Abel Daniel R. Kozlowski Frederick A. Fendel III President and CEO Chair of the Board Director and Chair of the Audit Committee Jeffrey G. Sheets Director Director Director and Chair of the Compensation Committee Director and Chair of the Nominating and Governance Committee I I I I I I I |

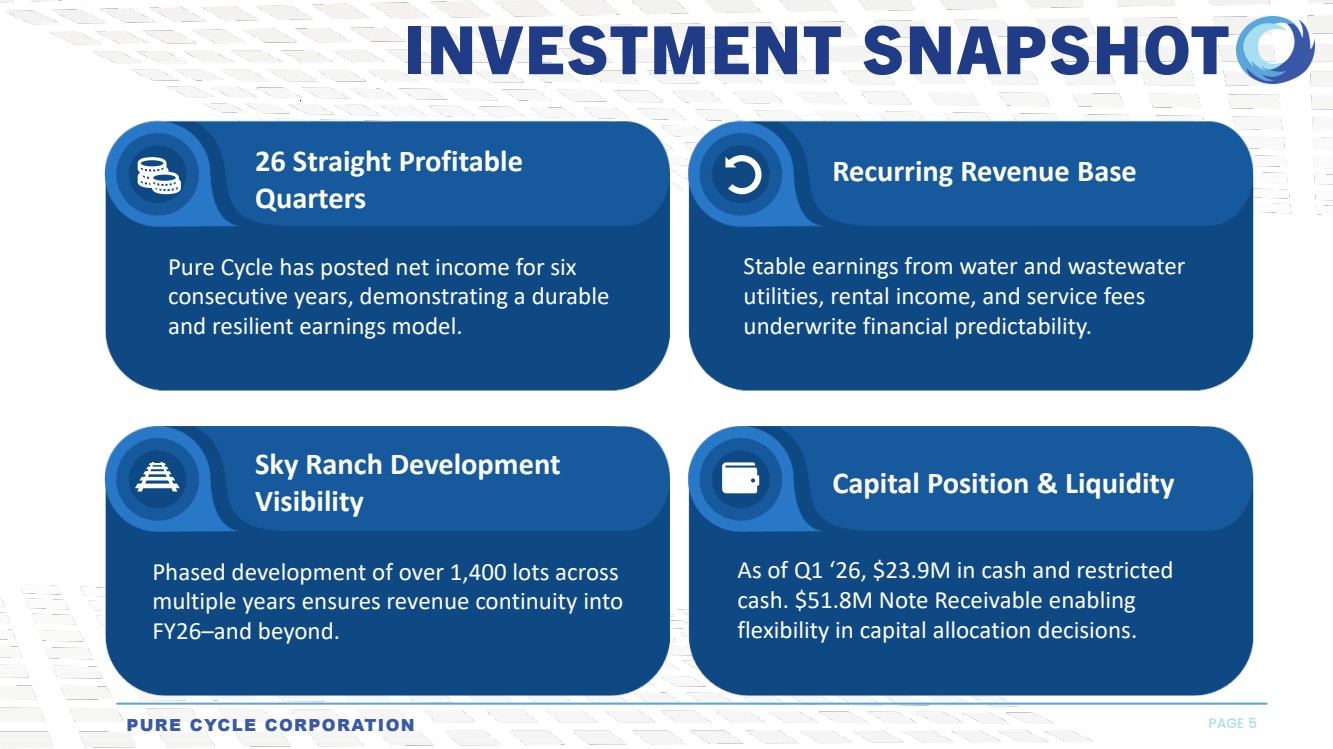

| INVESTMENT SNAPSHOT PURE CYCLE CORPORATION PAGE 5 Pure Cycle has posted net income for six consecutive years, demonstrating a durable and resilient earnings model. Stable earnings from water and wastewater utilities, rental income, and service fees underwrite financial predictability. As of Q1 ‘26, $23.9M in cash and restricted cash. $51.8M Note Receivable enabling flexibility in capital allocation decisions. Phased development of over 1,400 lots across multiple years ensures revenue continuity into FY26–and beyond. 26 Straight Profitable Quarters Recurring Revenue Base Sky Ranch Development Visibility Capital Position & Liquidity |

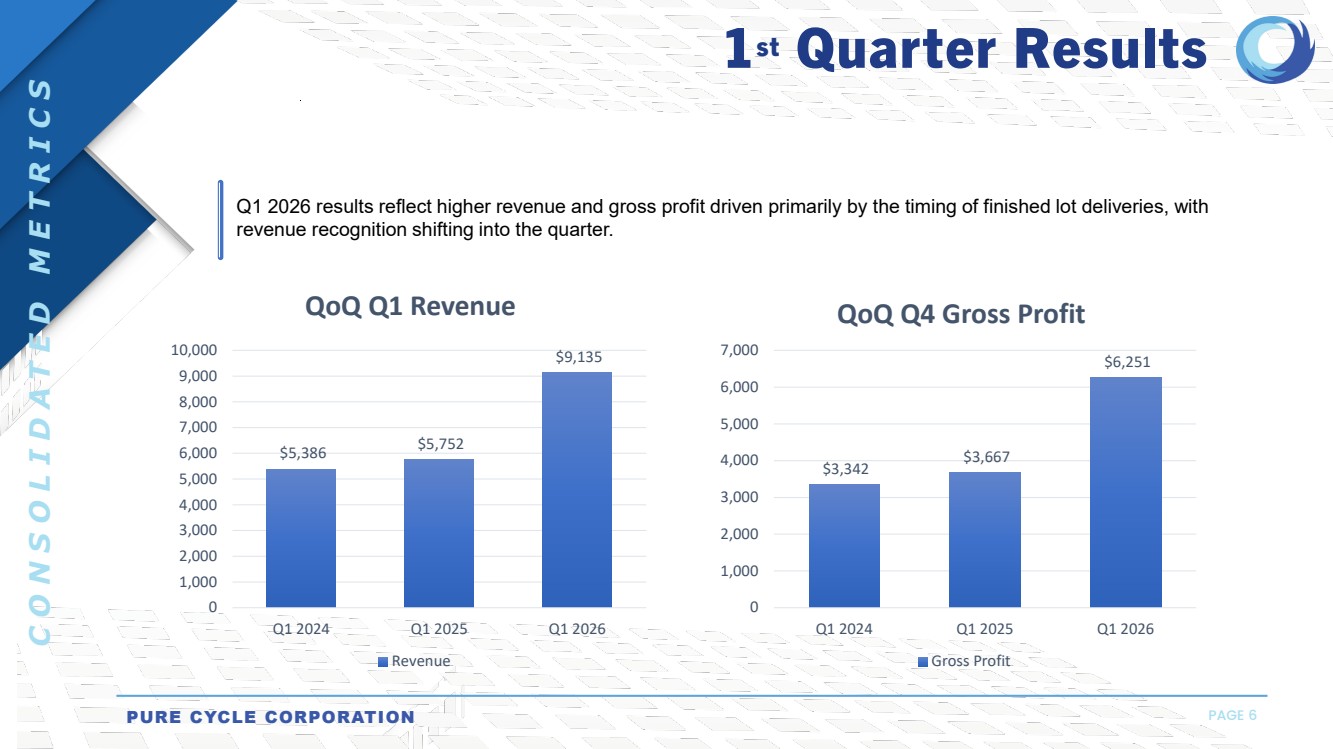

| 1st Quarter Results PURE CYCLE CORPORATION PAGE 6 CONSOLIDATED METRICS Q1 2026 results reflect higher revenue and gross profit driven primarily by the timing of finished lot deliveries, with revenue recognition shifting into the quarter. $5,386 $5,752 $9,135 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 Q1 2024 Q1 2025 Q1 2026 QoQ Q1 Revenue Revenue $3,342 $3,667 $6,251 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 Q1 2024 Q1 2025 Q1 2026 QoQ Q4 Gross Profit ■ ■ Gross Profit |

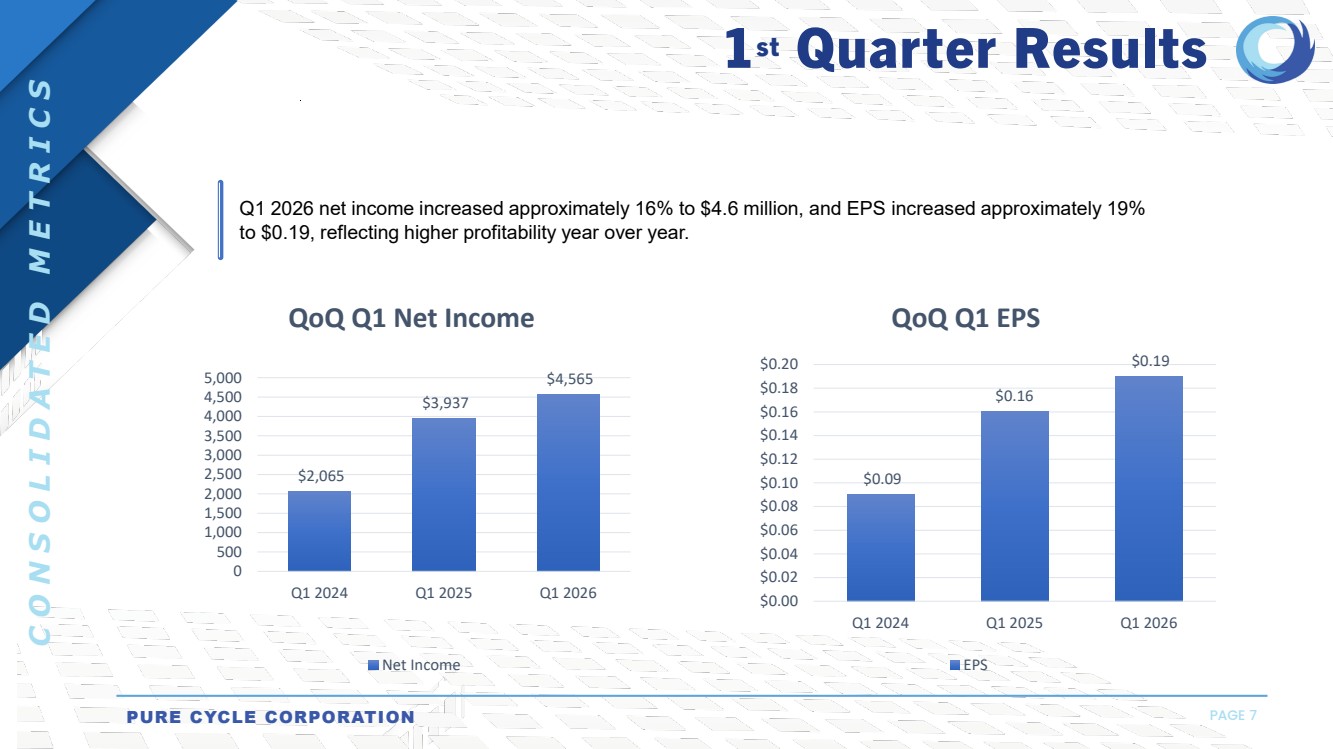

| PURE CYCLE CORPORATION PAGE 7 CONSOLIDATED METRICS Q1 2026 net income increased approximately 16% to $4.6 million, and EPS increased approximately 19% to $0.19, reflecting higher profitability year over year. $2,065 $3,937 $4,565 0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000 Q1 2024 Q1 2025 Q1 2026 QoQ Q1 Net Income Net Income $0.09 $0.16 $0.19 $0.00 $0.02 $0.04 $0.06 $0.08 $0.10 $0.12 $0.14 $0.16 $0.18 $0.20 Q1 2024 Q1 2025 Q1 2026 QoQ Q1 EPS EPS 1st Quarter Results ■ ■ |

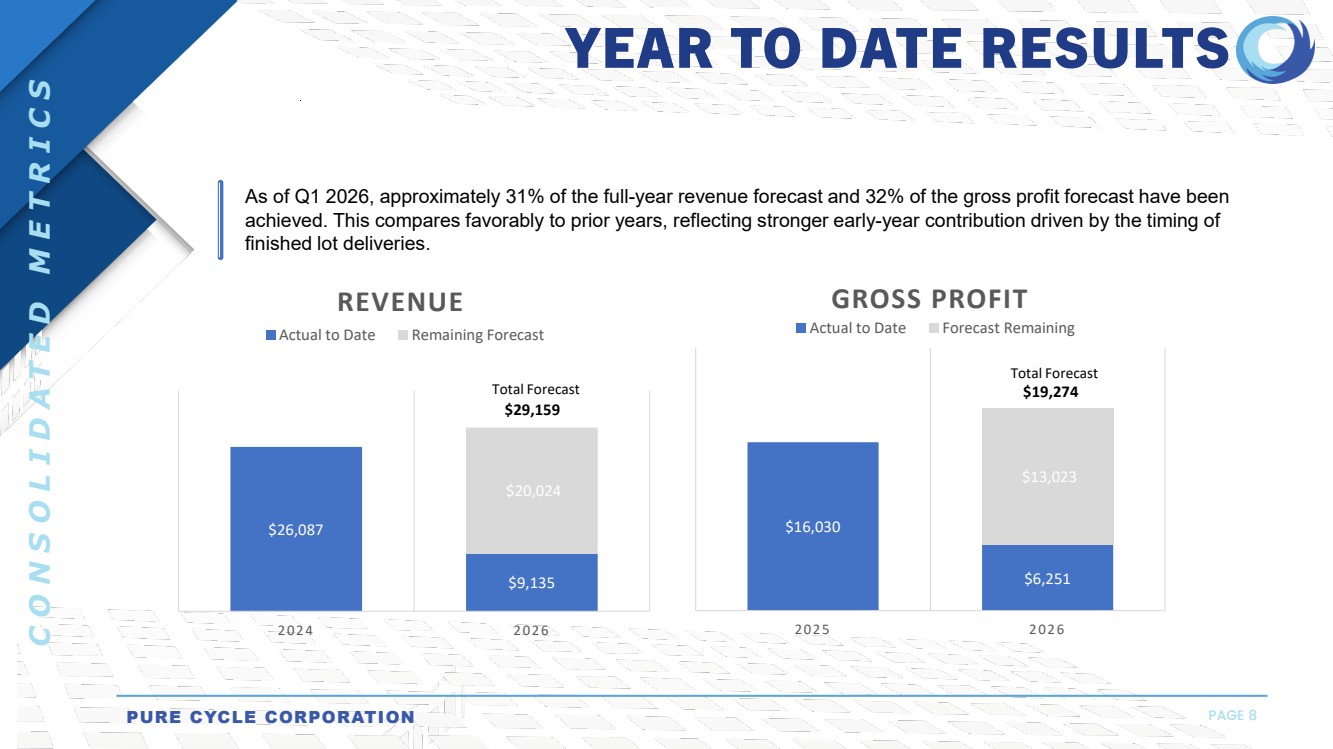

| YEAR TO DATE RESULTS PURE CYCLE CORPORATION PAGE 8 CONSOLIDATED METRICS As of Q1 2026, approximately 31% of the full-year revenue forecast and 32% of the gross profit forecast have been achieved. This compares favorably to prior years, reflecting stronger early-year contribution driven by the timing of finished lot deliveries. $26,087 $9,135 $20,024 $29,159 2024 2026 REVENUE Actual to Date Remaining Forecast Total Forecast $16,030 $6,251 $13,023 $19,274 2025 2026 GROSS PROFIT Actual to Date Forecast Remaining Total Forecast ■ ■ ■ ■ |

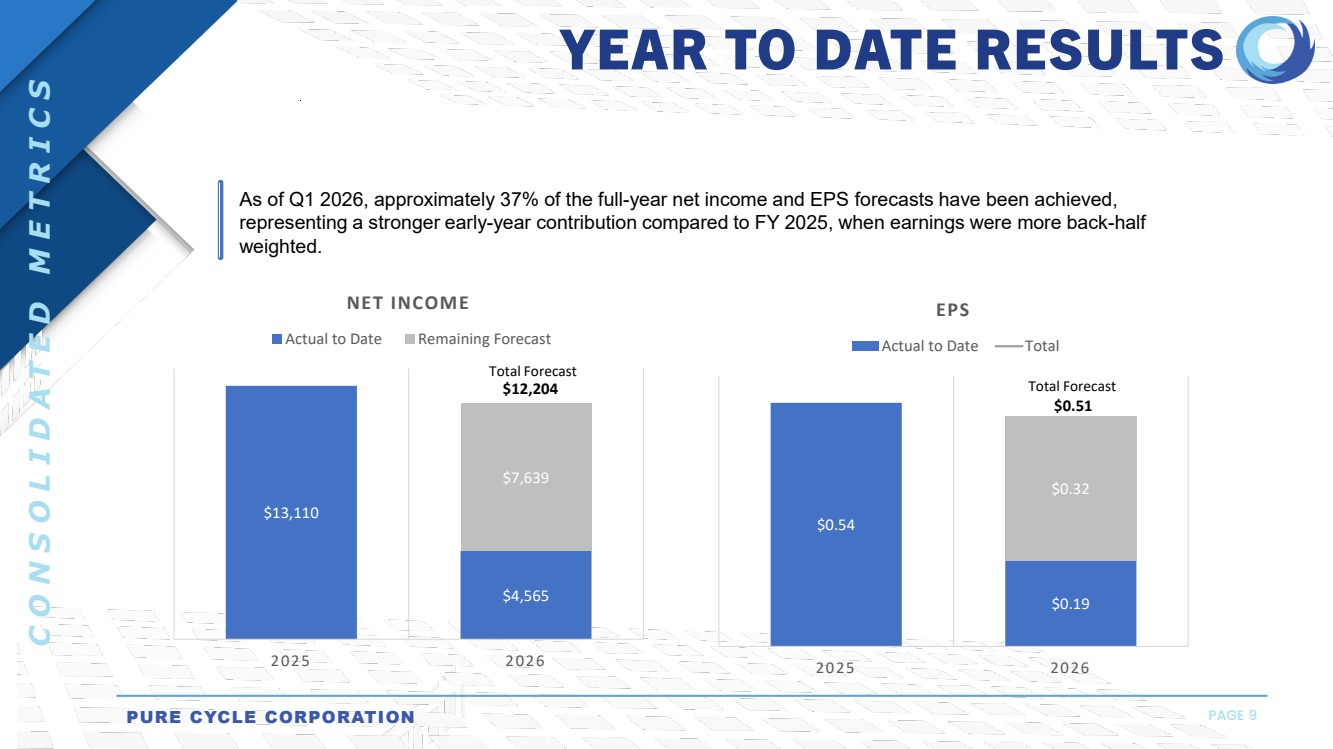

| YEAR TO DATE RESULTS PURE CYCLE CORPORATION PAGE 9 CONSOLIDATED METRICS As of Q1 2026, approximately 37% of the full-year net income and EPS forecasts have been achieved, representing a stronger early-year contribution compared to FY 2025, when earnings were more back-half weighted. $13,110 $4,565 $7,639 $12,204 2025 2026 NET INCOME Actual to Date Remaining Forecast Total Forecast $0.54 $0.19 $0.32 $0.51 2025 2026 EPS Actual to Date Total Total Forecast ■ ■ - - |

| Water Utilities |

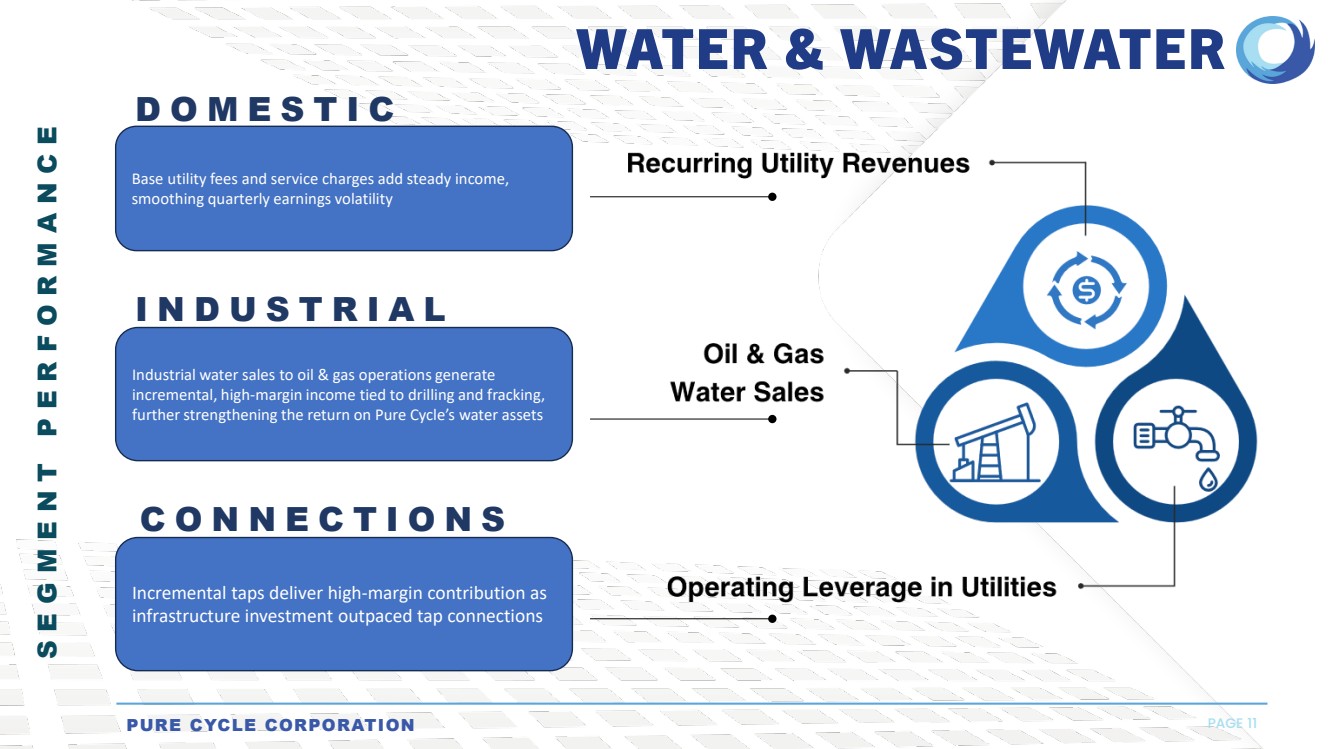

| Base utility fees and service charges add steady income, smoothing quarterly earnings volatility Industrial water sales to oil & gas operations generate incremental, high-margin income tied to drilling and fracking, further strengthening the return on Pure Cycle’s water assets Incremental taps deliver high-margin contribution as infrastructure investment outpaced tap connections WATER & WASTEWATER SEGMENT PERFORMANCE PURE CYCLE CORPORATION PAGE 11 DOMESTIC INDUSTRIAL CONNECTIONS Recurring Utillity Revenues 011 & Gas Water Sales Operating Leverage in Utilities |

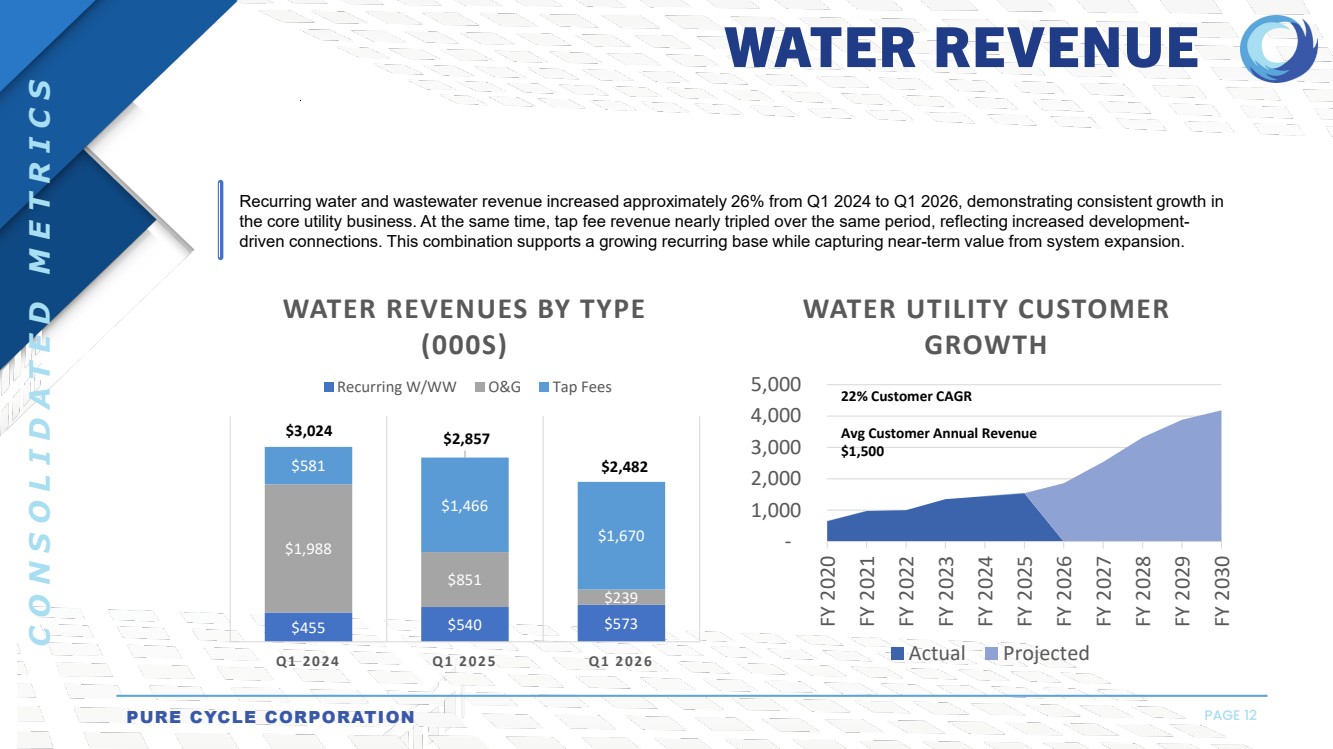

| WATER REVENUE PURE CYCLE CORPORATION PAGE 12 CONSOLIDATED METRICS - 1,000 2,000 3,000 4,000 5,000 FY 2020 FY 2021 FY 2022 FY 2023 FY 2024 FY 2025 FY 2026 FY 2027 FY 2028 FY 2029 FY 2030 WATER UTILITY CUSTOMER GROWTH Actual Projected $455 $540 $573 $1,988 $851 $239 $581 $1,466 $1,670 $3,024 $2,857 $2,482 Q1 2024 Q1 2025 Q1 2026 WATER REVENUES BY TYPE (000S) Recurring W/WW O&G Tap Fees 22% Customer CAGR Avg Customer Annual Revenue $1,500 Recurring water and wastewater revenue increased approximately 26% from Q1 2024 to Q1 2026, demonstrating consistent growth in the core utility business. At the same time, tap fee revenue nearly tripled over the same period, reflecting increased development-driven connections. This combination supports a growing recurring base while capturing near-term value from system expansion. ■ ■ ■ ■ ■ |

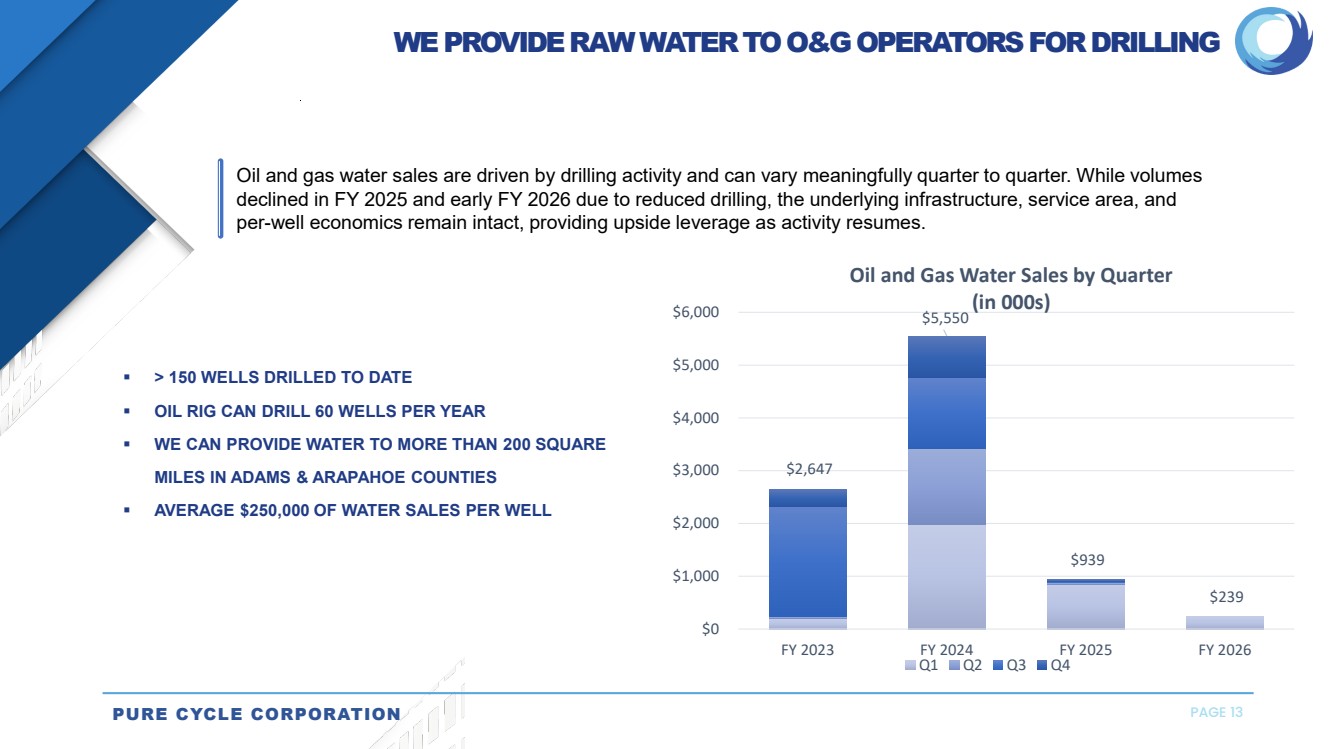

| PURE CYCLE CORPORATION PAGE 13 $2,647 $5,550 $939 $239 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 FY 2023 FY 2024 FY 2025 FY 2026 Oil and Gas Water Sales by Quarter (in 000s) Q1 Q2 Q3 Q4 > 150 WELLS DRILLED TO DATE OIL RIG CAN DRILL 60 WELLS PER YEAR WE CAN PROVIDE WATER TO MORE THAN 200 SQUARE MILES IN ADAMS & ARAPAHOE COUNTIES AVERAGE $250,000 OF WATER SALES PER WELL WE PROVIDE RAW WATER TO O&G OPERATORS FOR DRILLING Oil and gas water sales are driven by drilling activity and can vary meaningfully quarter to quarter. While volumes declined in FY 2025 and early FY 2026 due to reduced drilling, the underlying infrastructure, service area, and per-well economics remain intact, providing upside leverage as activity resumes. ■ ■ ■ ■ |

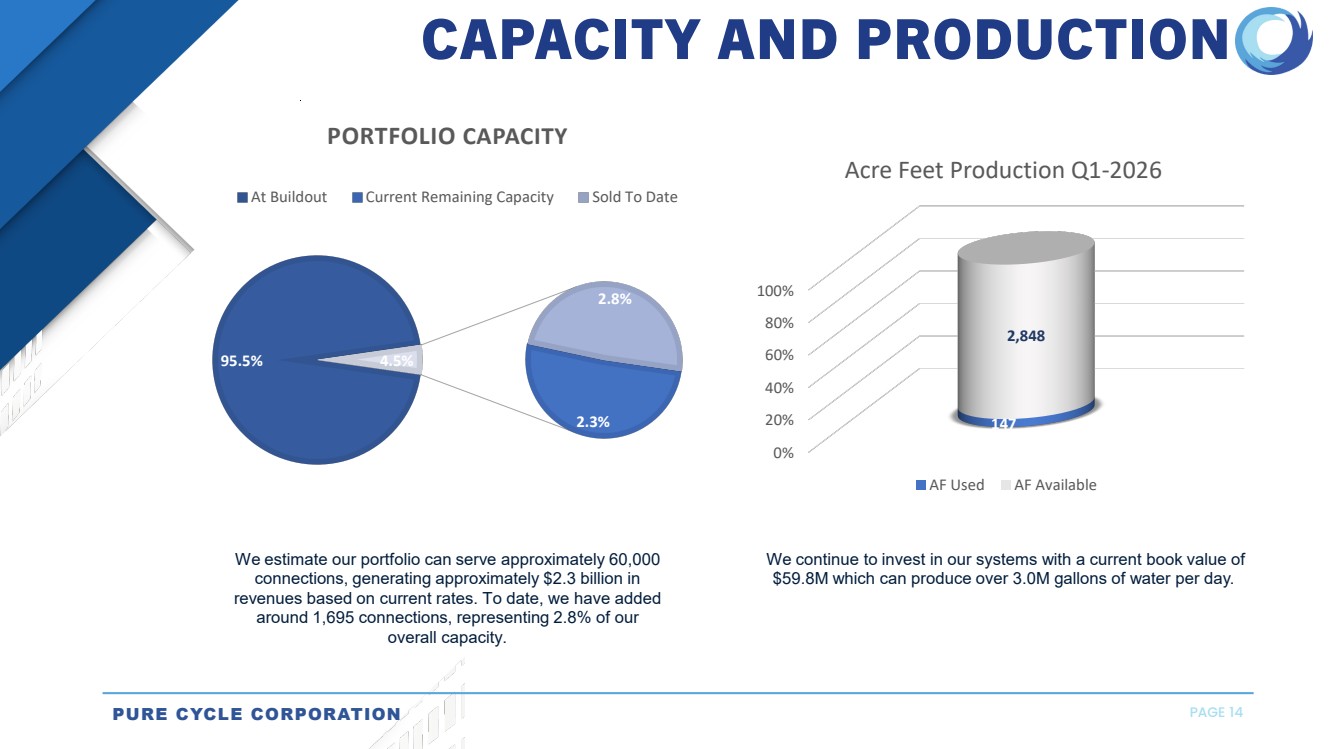

| PURE CYCLE CORPORATION PAGE 14 We continue to invest in our systems with a current book value of $59.8M which can produce over 3.0M gallons of water per day. We estimate our portfolio can serve approximately 60,000 connections, generating approximately $2.3 billion in revenues based on current rates. To date, we have added around 1,695 connections, representing 2.8% of our overall capacity. 95.5% 2.3% 2.8% 4.5% PORTFOLIO CAPACITY At Buildout Current Remaining Capacity Sold To Date CAPACITY AND PRODUCTION 0% 20% 40% 60% 80% 100% 147 2,848 Acre Feet Production Q1-2026 AF Used AF Available ■ ■ , , ,, , , , , _,,/ , , , , ,, ,, , ■ |

| Land Development |

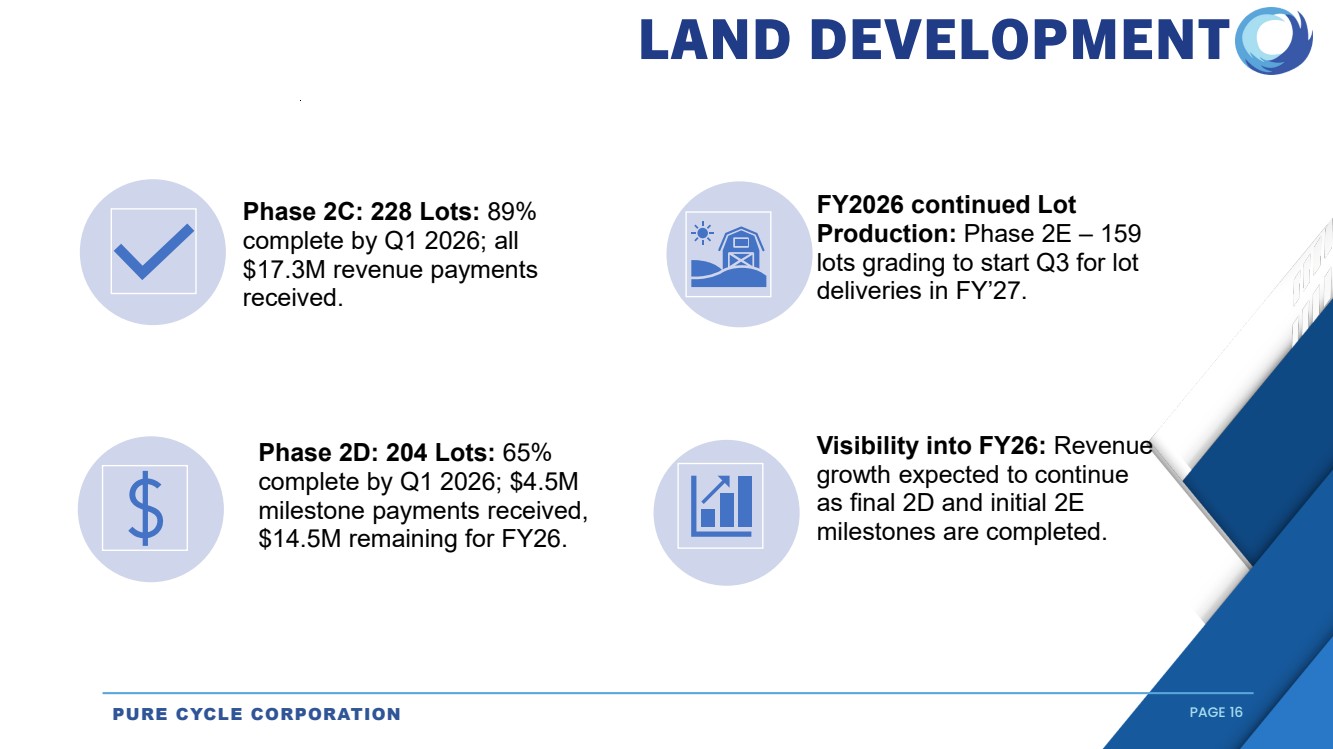

| PURE CYCLE CORPORATION PAGE 16 LAND DEVELOPMENT Phase 2D: 204 Lots: 65% complete by Q1 2026; $4.5M milestone payments received, $14.5M remaining for FY26. Visibility into FY26: Revenue growth expected to continue as final 2D and initial 2E milestones are completed. FY2026 continued Lot Production: Phase 2E – 159 lots grading to start Q3 for lot deliveries in FY’27. Phase 2C: 228 Lots: 89% complete by Q1 2026; all $17.3M revenue payments received. |

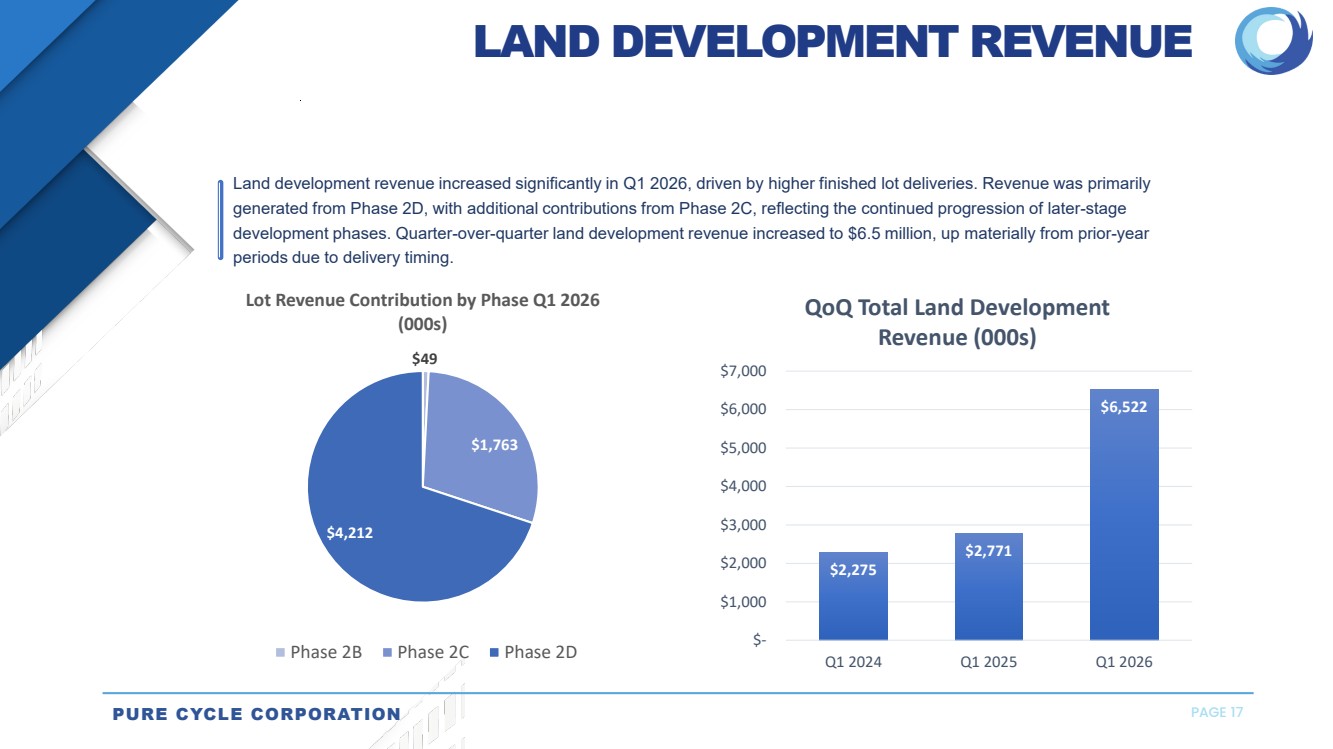

| PURE CYCLE CORPORATION PAGE 17 LAND DEVELOPMENT REVENUE $2,275 $2,771 $6,522 $- $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 Q1 2024 Q1 2025 Q1 2026 QoQ Total Land Development Revenue (000s) $49 $1,763 $4,212 Lot Revenue Contribution by Phase Q1 2026 (000s) Phase 2B Phase 2C Phase 2D Land development revenue increased significantly in Q1 2026, driven by higher finished lot deliveries. Revenue was primarily generated from Phase 2D, with additional contributions from Phase 2C, reflecting the continued progression of later-stage development phases. Quarter-over-quarter land development revenue increased to $6.5 million, up materially from prior-year periods due to delivery timing. ■ ■ ■ |

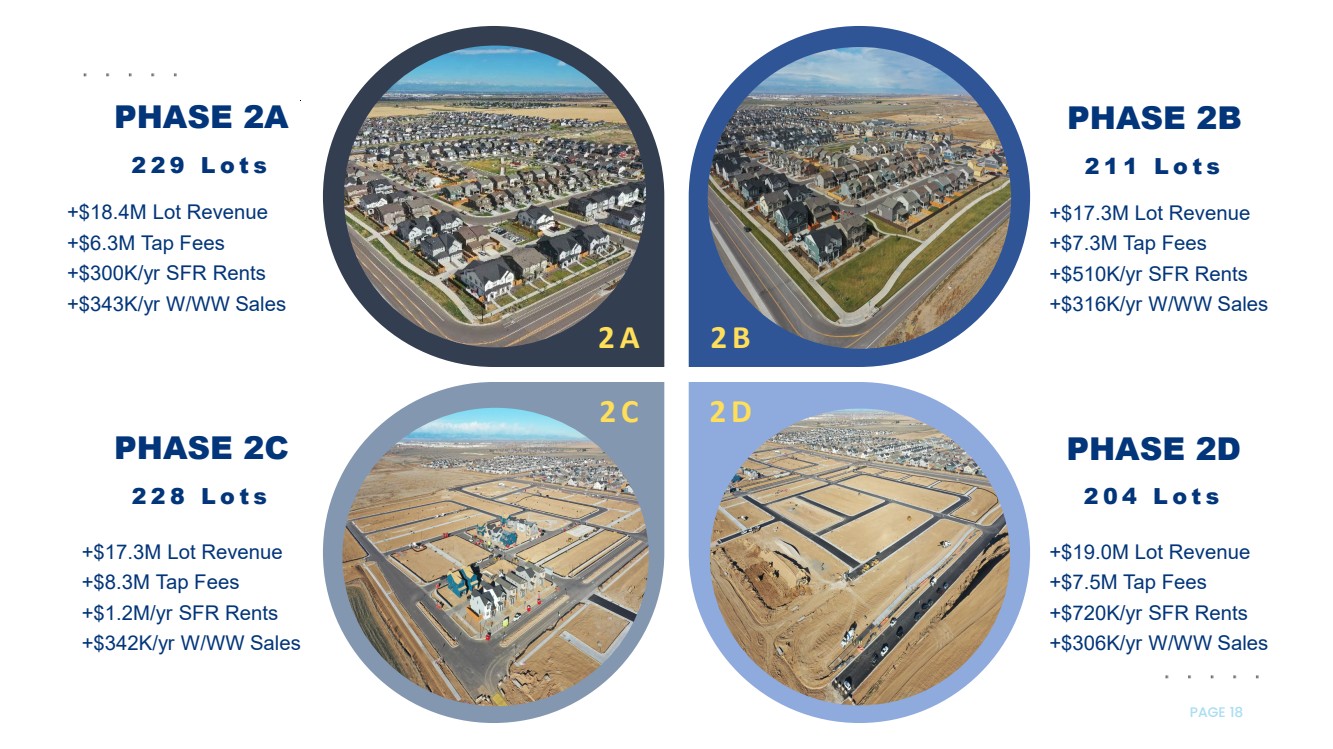

| PAGE 18 2 A +$18.4M Lot Revenue +$6.3M Tap Fees +$300K/yr SFR Rents +$343K/yr W/WW Sales PHASE 2A 229 Lots 2 B +$17.3M Lot Revenue +$7.3M Tap Fees +$510K/yr SFR Rents +$316K/yr W/WW Sales 2 C 2 D +$19.0M Lot Revenue +$7.5M Tap Fees +$720K/yr SFR Rents +$306K/yr W/WW Sales PHASE 2B 211 Lots PHASE 2C 228 Lots PHASE 2D 204 Lots +$17.3M Lot Revenue +$8.3M Tap Fees +$1.2M/yr SFR Rents +$342K/yr W/WW Sales |

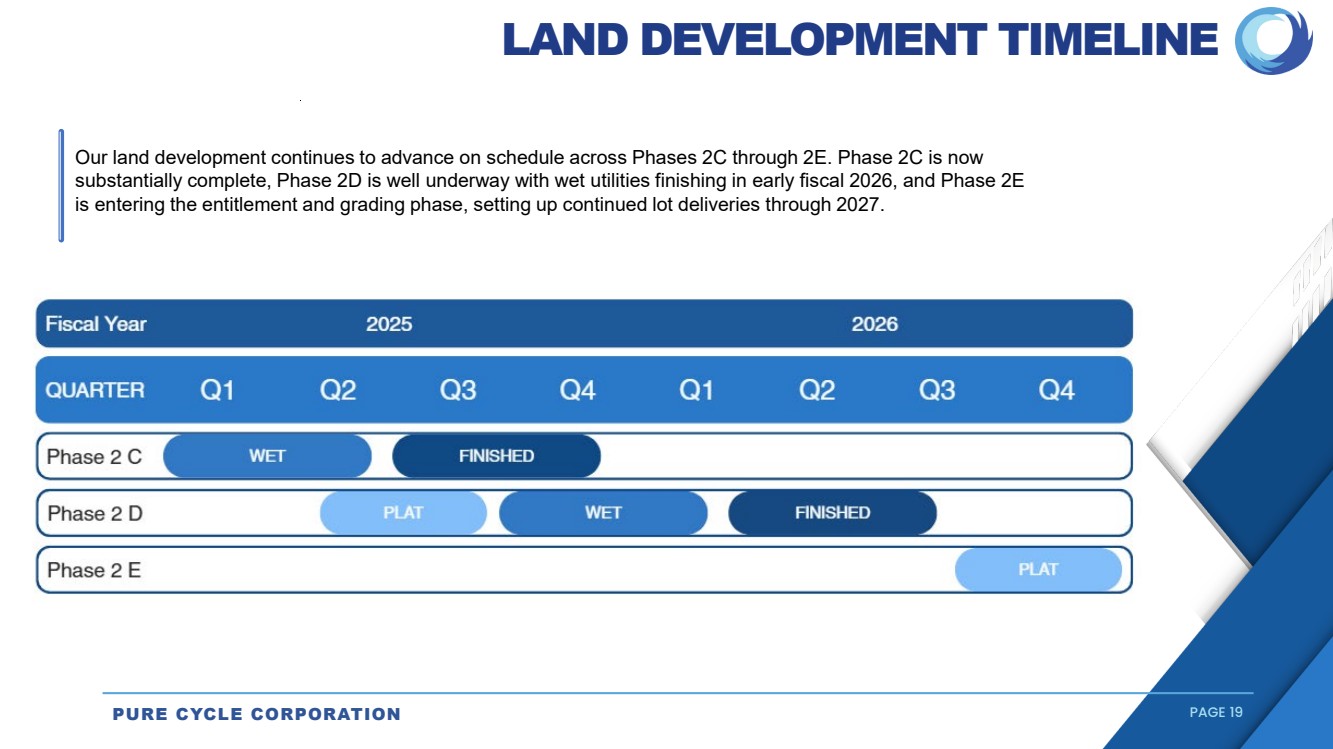

| PURE CYCLE CORPORATION PAGE 19 LAND DEVELOPMENT TIMELINE Our land development continues to advance on schedule across Phases 2C through 2E. Phase 2C is now substantially complete, Phase 2D is well underway with wet utilities finishing in early fiscal 2026, and Phase 2E is entering the entitlement and grading phase, setting up continued lot deliveries through 2027. Fiscal Year 2025 2026 QUARTER Q1 Q2 Q3 Q4 Q1 Q2 Q3, 1 Q,4 Phase 2 C ANISHED Phase 2 D WET I ANISHED (Phase 2 E D |

| This phase will add an estimated • $14M Lot Revenue • $4.3M Tap Fees • $300K/yr SFR Rents • $225K/yr W/WW Sales PHASE 2E 159 Lots PURE CYCLE CORPORATION PAGE 20 |

| Pg. 21 GROUNDBREAKING ON HIGH SCHOOL PURE CYCLE CORPORATION PAGE 21 |

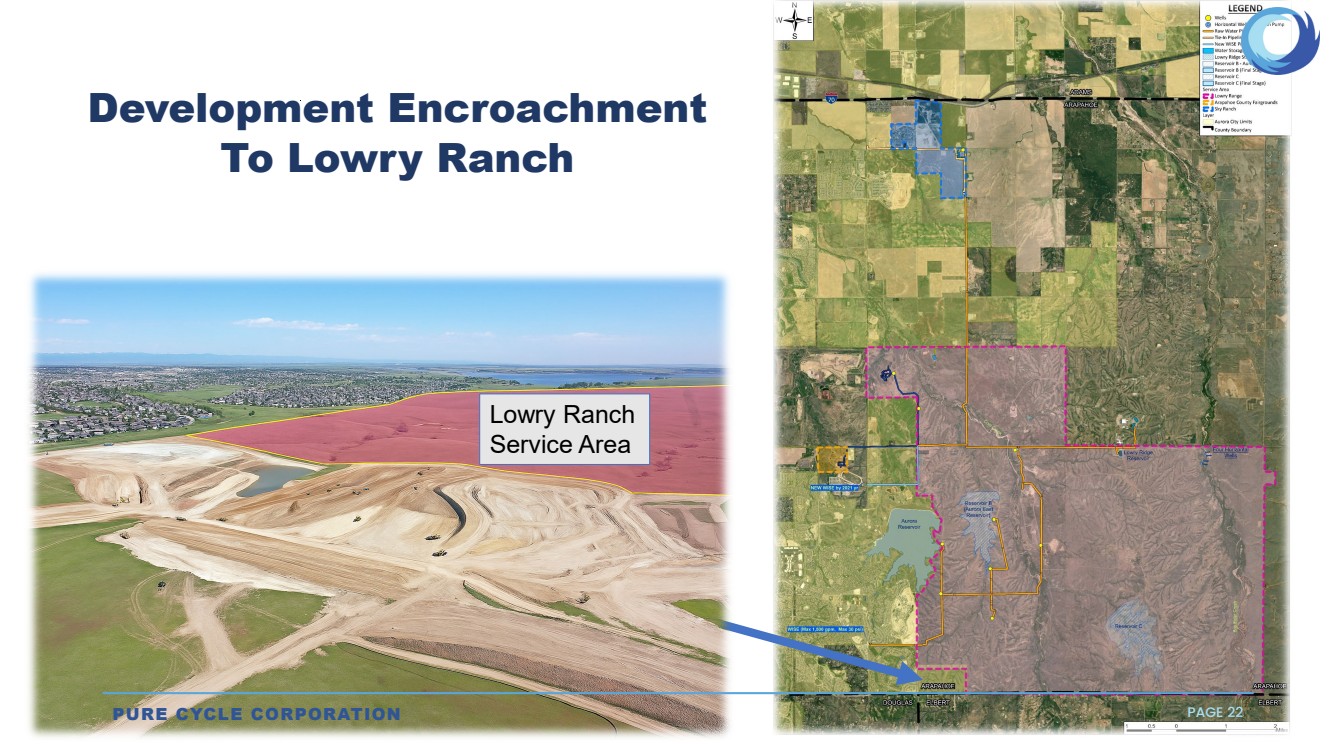

| Pg. 22 Development Encroachment To Lowry Ranch PURE CYCLE CORPORATION PAGE 22 Lowry Ranch Service Area -,,,,~,,...,- - WaterStor.ig ~ Lowry RidgeS [:JReservoirS-Au c=] ReserY<JirS(FinalSt c::J ReservolrC c:J ReservoirC(Final Stage) Servlce Afea C' ,I Lowry Range C,IAr.ip.,hoeCountyFairgrounds C'.I SkvRanch ~ ... , |

| Single-Family Rentals |

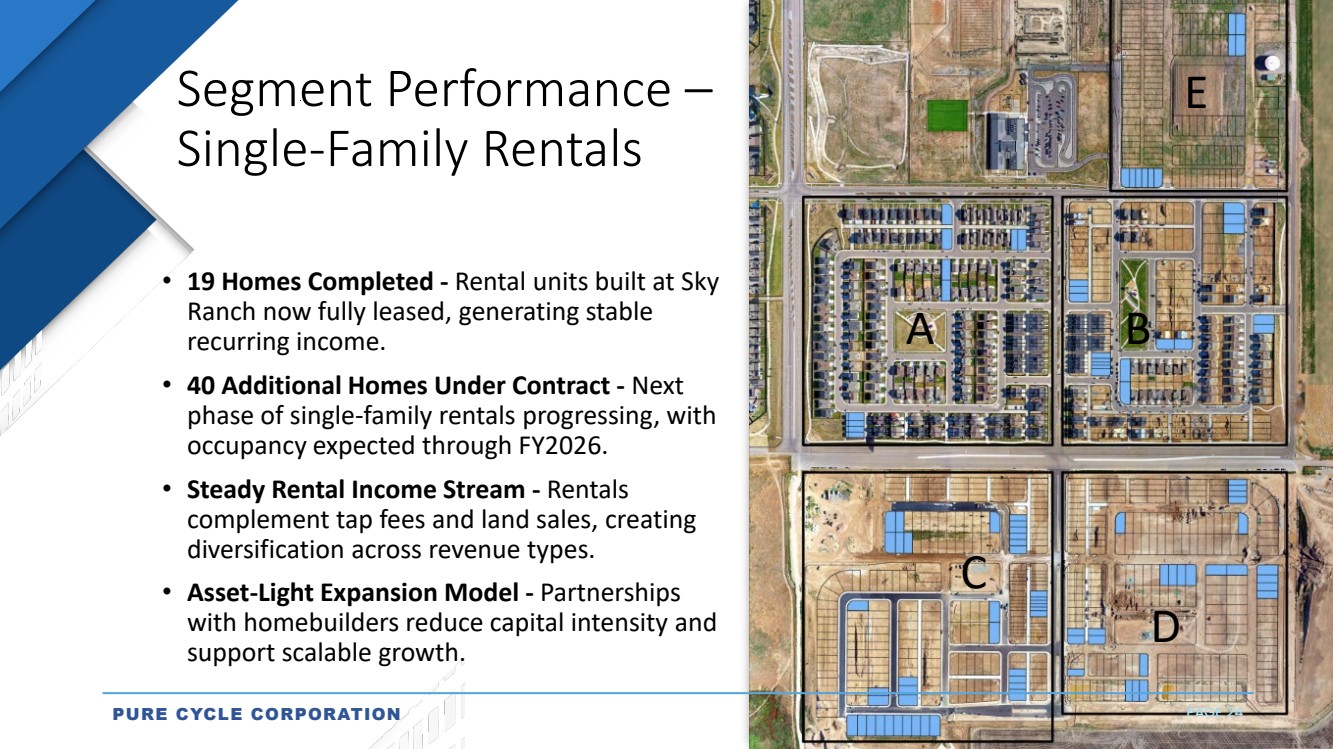

| PURE CYCLE CORPORATION PAGE 24 Segment Performance – Single-Family Rentals • 19 Homes Completed - Rental units built at Sky Ranch now fully leased, generating stable recurring income. • 40 Additional Homes Under Contract - Next phase of single-family rentals progressing, with occupancy expected through FY2026. • Steady Rental Income Stream - Rentals complement tap fees and land sales, creating diversification across revenue types. • Asset-Light Expansion Model - Partnerships with homebuilders reduce capital intensity and support scalable growth. A B C D E |

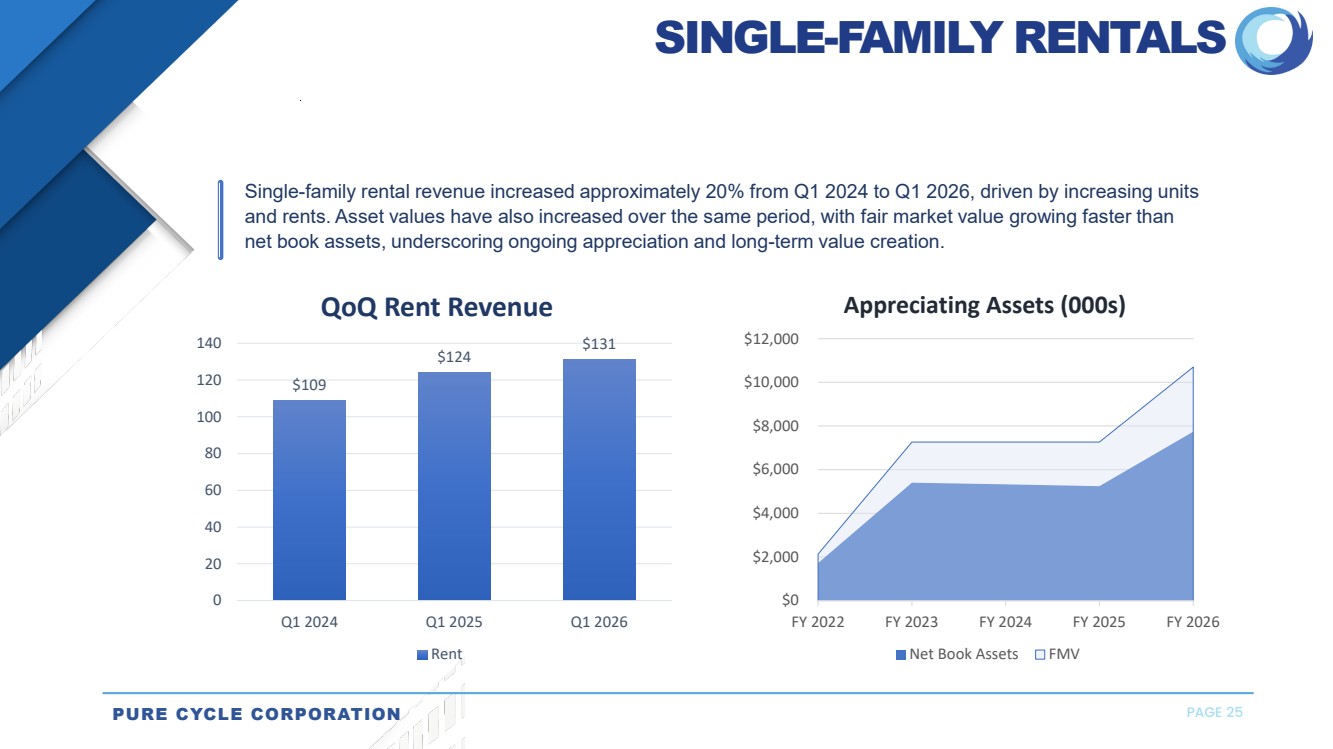

| PURE CYCLE CORPORATION PAGE 25 Single-family rental revenue increased approximately 20% from Q1 2024 to Q1 2026, driven by increasing units and rents. Asset values have also increased over the same period, with fair market value growing faster than net book assets, underscoring ongoing appreciation and long-term value creation. SINGLE-FAMILY RENTALS $109 $124 $131 0 20 40 60 80 100 120 140 Q1 2024 Q1 2025 Q1 2026 QoQ Rent Revenue Rent $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 FY 2022 FY 2023 FY 2024 FY 2025 FY 2026 Appreciating Assets (000s) ■ ■ Net Book Assets □ FMV |

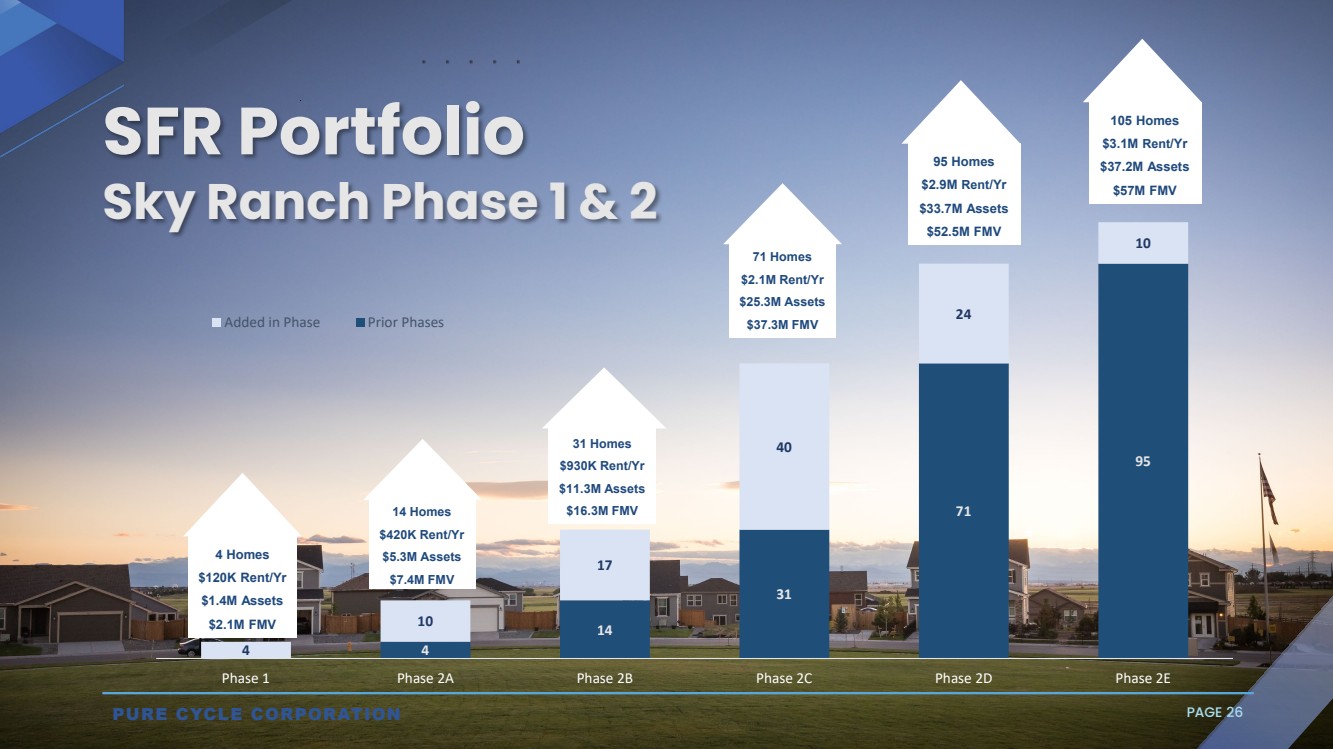

| 4 14 31 71 95 4 10 17 40 24 10 Phase 1 Phase 2A Phase 2B Phase 2C Phase 2D Phase 2E Added in Phase Prior Phases 14 Homes $420K Rent/Yr $5.3M Assets $7.4M FMV 31 Homes $930K Rent/Yr $11.3M Assets $16.3M FMV 71 Homes $2.1M Rent/Yr $25.3M Assets $37.3M FMV 4 Homes $120K Rent/Yr $1.4M Assets $2.1M FMV 95 Homes $2.9M Rent/Yr $33.7M Assets $52.5M FMV SFR Portfolio Sky Ranch Phase 1 & 2 105 Homes $3.1M Rent/Yr $37.2M Assets $57M FMV PURE CYCLE CORPORATION PAGE 26 |

| Capital Allocation & Shareholder Value |

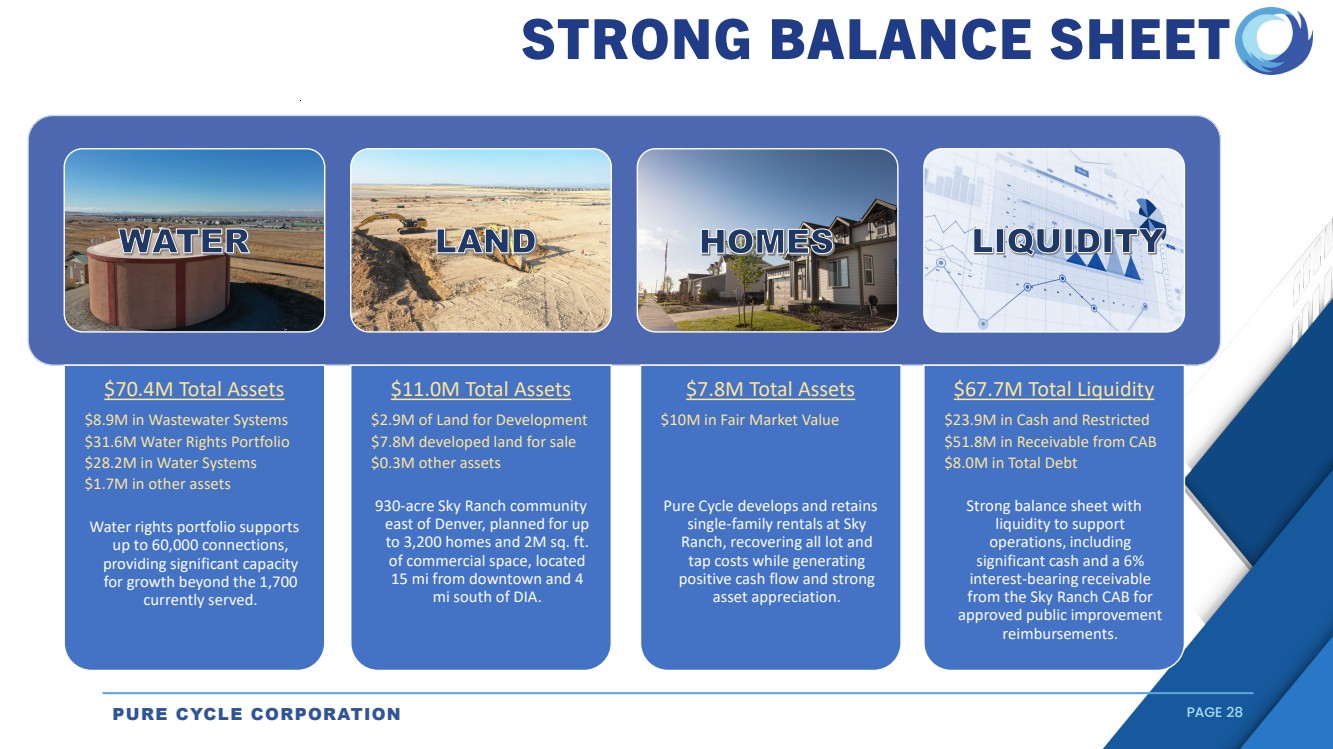

| PURE CYCLE CORPORATION PAGE 28 $70.4M Total Assets $8.9M in Wastewater Systems $31.6M Water Rights Portfolio $28.2M in Water Systems $1.7M in other assets Water rights portfolio supports up to 60,000 connections, providing significant capacity for growth beyond the 1,700 currently served. $11.0M Total Assets $2.9M of Land for Development $7.8M developed land for sale $0.3M other assets 930-acre Sky Ranch community east of Denver, planned for up to 3,200 homes and 2M sq. ft. of commercial space, located 15 mi from downtown and 4 mi south of DIA. $7.8M Total Assets $10M in Fair Market Value Pure Cycle develops and retains single-family rentals at Sky Ranch, recovering all lot and tap costs while generating positive cash flow and strong asset appreciation. $67.7M Total Liquidity $23.9M in Cash and Restricted $51.8M in Receivable from CAB $8.0M in Total Debt Strong balance sheet with liquidity to support operations, including significant cash and a 6% interest-bearing receivable from the Sky Ranch CAB for approved public improvement reimbursements. STRONG BALANCE SHEET ll&U . ., . . ~ . : . . . |

| Recurring Revenue Strength Utilities Revenue Stability: Recurring water and wastewater revenue offer consistent contribution across cycles Rental Income from 19 Homes: Fully leased homes generating monthly cash flows; 5 units coming online in Q2 and an additional 40 units to expand income in FY26 Diversified Earnings Mix: Blending utility income with residential rent yields lowers overall earnings volatility and cash flows SFR Synergy with Land Development: Rental strategy monetizes lots internally, capturing additional value from Sky Ranch development PURE CYCLE CORPORATION PAGE 29 ~ |

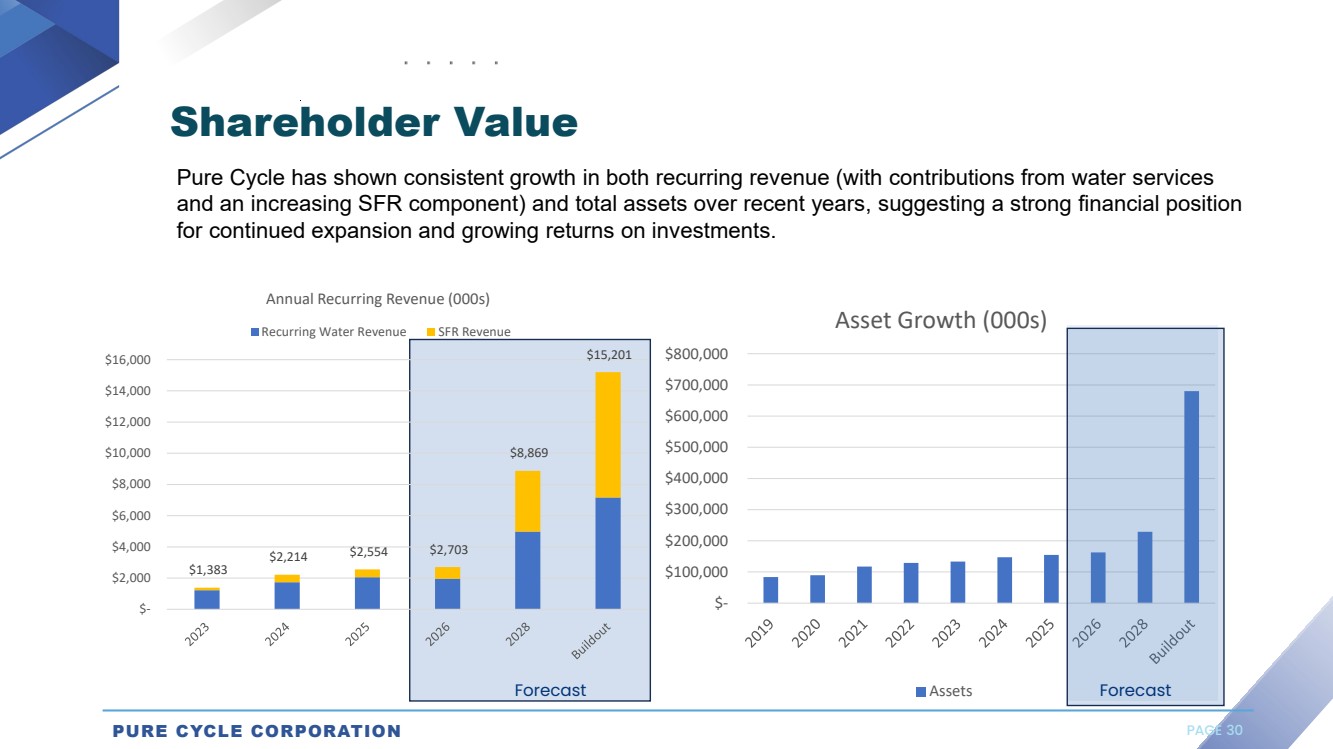

| $- $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 Asset Growth (000s) Assets Shareholder Value Pure Cycle has shown consistent growth in both recurring revenue (with contributions from water services and an increasing SFR component) and total assets over recent years, suggesting a strong financial position for continued expansion and growing returns on investments. Forecast Forecast $1,383 $2,214 $2,554 $2,703 $8,869 $15,201 $- $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 Annual Recurring Revenue (000s) Recurring Water Revenue SFR Revenue PURE CYCLE CORPORATION PAGE 30 ■ ■ I I I I I I I I I ■ I I I I I I I I I ~ & ci,'> ci,'<> ci,'b ~ '\,\) '\,\) '\,\) '\,\) '\,\) -~~o ,;y- <o ~ (\,~ 0,">- 0,'\- cc, ~ ~ 0,<o 0,Cb ~ '\,~ '\,~ '\,~ '\,~ '\,~ '\,~ '\,~ '\,~ '\,~ . 'oo <o ~ ■ |

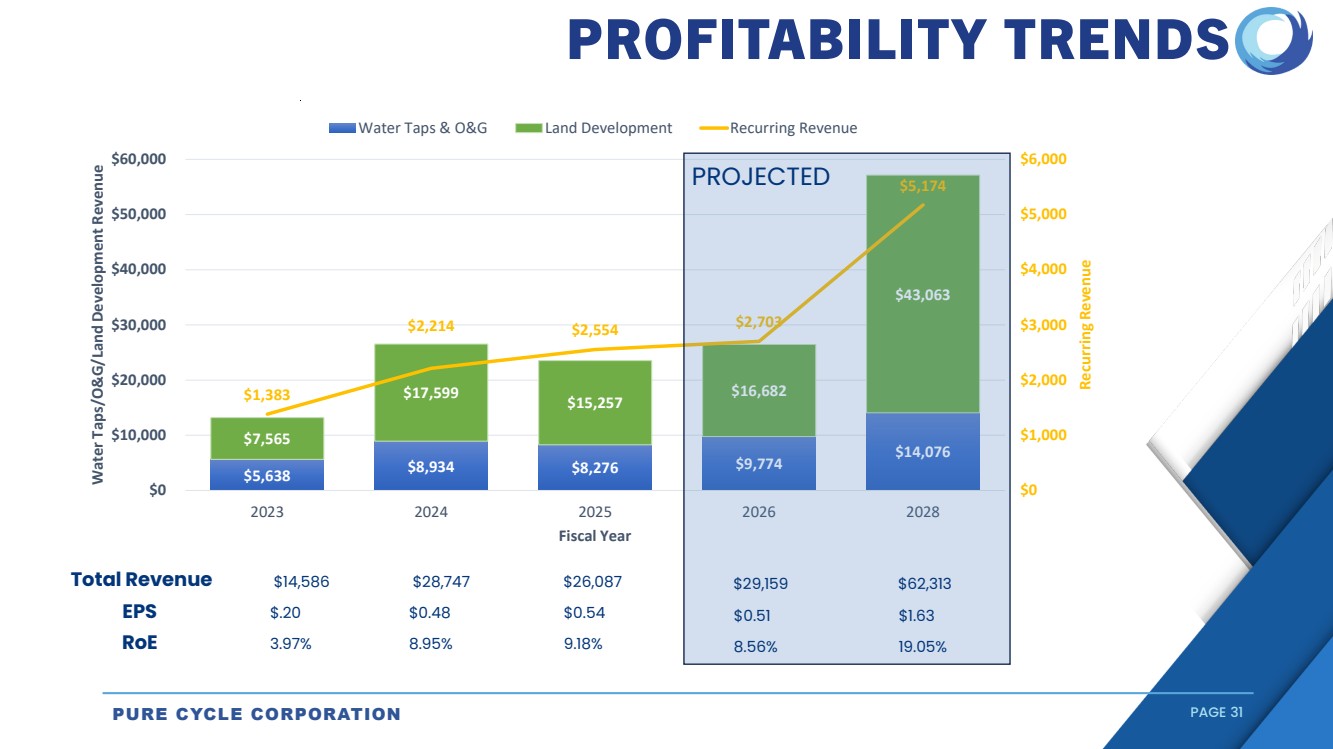

| PURE CYCLE CORPORATION PAGE 31 $5,638 $8,934 $8,276 $9,774 $14,076 $7,565 $17,599 $15,257 $16,682 $43,063 $1,383 $2,214 $2,554 $2,703 $5,174 $0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $0 $10,000 $20,000 $30,000 $40,000 $50,000 $60,000 2023 2024 2025 2026 2028 Recurring Revenue Water Taps/O&G/Land Development Revenue Fiscal Year Water Taps & O&G Land Development Recurring Revenue $.20 $0.48 RoE 3.97% 8.95% $0.54 9.18% $0.51 8.56% $1.63 19.05% EPS Total Revenue $14,586 $28,747 $26,087 $29,159 $62,313 PROJECTED PROFITABILITY TRENDS - - |

| PURE CYCLE CORPORATION PAGE 32 FY26 Gross Revenue: $26–30M Range: Scenario modeling based on timing of Phase 2D/2E milestone completions and builder uptake. FY26 EPS Sensitivity: $0.43–$0.52: EPS estimates vary with lot closings pace and rental unit lease-up timing. Upside in Timing Acceleration: If delivery milestones pull into early FY26, potential for beat vs baseline estimates. Valuation Sensitivity Scenarios |

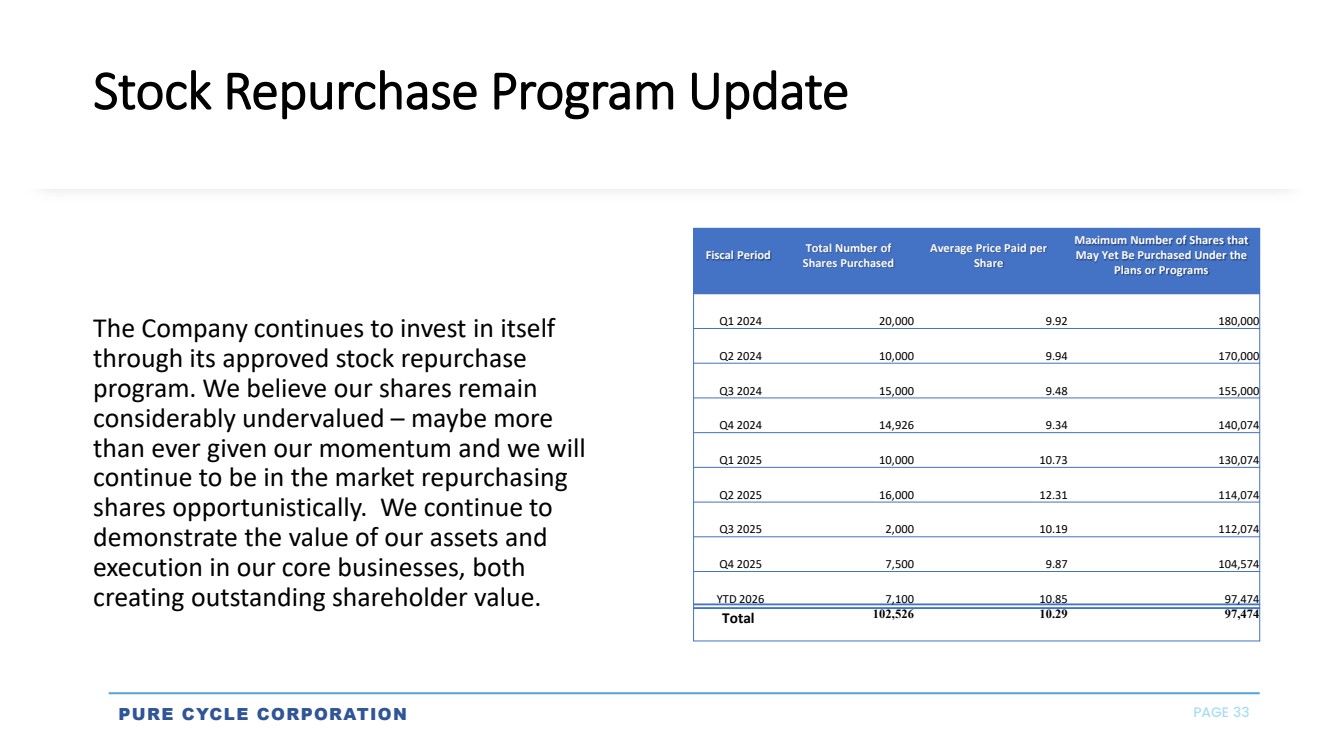

| Stock Repurchase Program Update The Company continues to invest in itself through its approved stock repurchase program. We believe our shares remain considerably undervalued – maybe more than ever given our momentum and we will continue to be in the market repurchasing shares opportunistically. We continue to demonstrate the value of our assets and execution in our core businesses, both creating outstanding shareholder value. Fiscal Period Total Number of Shares Purchased Average Price Paid per Share Maximum Number of Shares that May Yet Be Purchased Under the Plans or Programs Q1 2024 20,000 9.92 180,000 Q2 2024 10,000 9.94 170,000 Q3 2024 15,000 9.48 155,000 Q4 2024 14,926 9.34 140,074 Q1 2025 10,000 10.73 130,074 Q2 2025 16,000 12.31 114,074 Q3 2025 2,000 10.19 112,074 Q4 2025 7,500 9.87 104,574 YTD 2026 7,100 10.85 97,474 Total 102,526 10.29 97,474 PURE CYCLE CORPORATION PAGE 33 |

| Short-Term (3–5 Years) • Water Utilities: Customer base expected to grow to ~2,500 accounts with consistent tap sales across remaining Sky Ranch phases. Base utility fees and service charges continue to provide predictable, recurring revenue, with annual tap fee increases of ~3%. • Land Development: Ongoing lot deliveries and steady absorption at Sky Ranch drive near-term growth. Lot margins are expected to remain healthy as costs stabilize, with commercial parcels set through completion of Interchange to monetize providing additional upside. • Single-Family Rentals: Expansion to more than 100 homes as the segment scales, benefiting from suburban population growth and sustained housing demand. Efficiencies improve as operations mature and occupancy remains strong. PURE CYCLE CORPORATION PAGE 35 Legend 8 - - = Existing Right-of-Way v-v = Retaining Wall ---- = Bridge Railing Colfax Avenue / --- /i / / - -- 1:-r-~ I 1 -~ I I -- I --- ----------- -~ ---.....: -----......: --- |

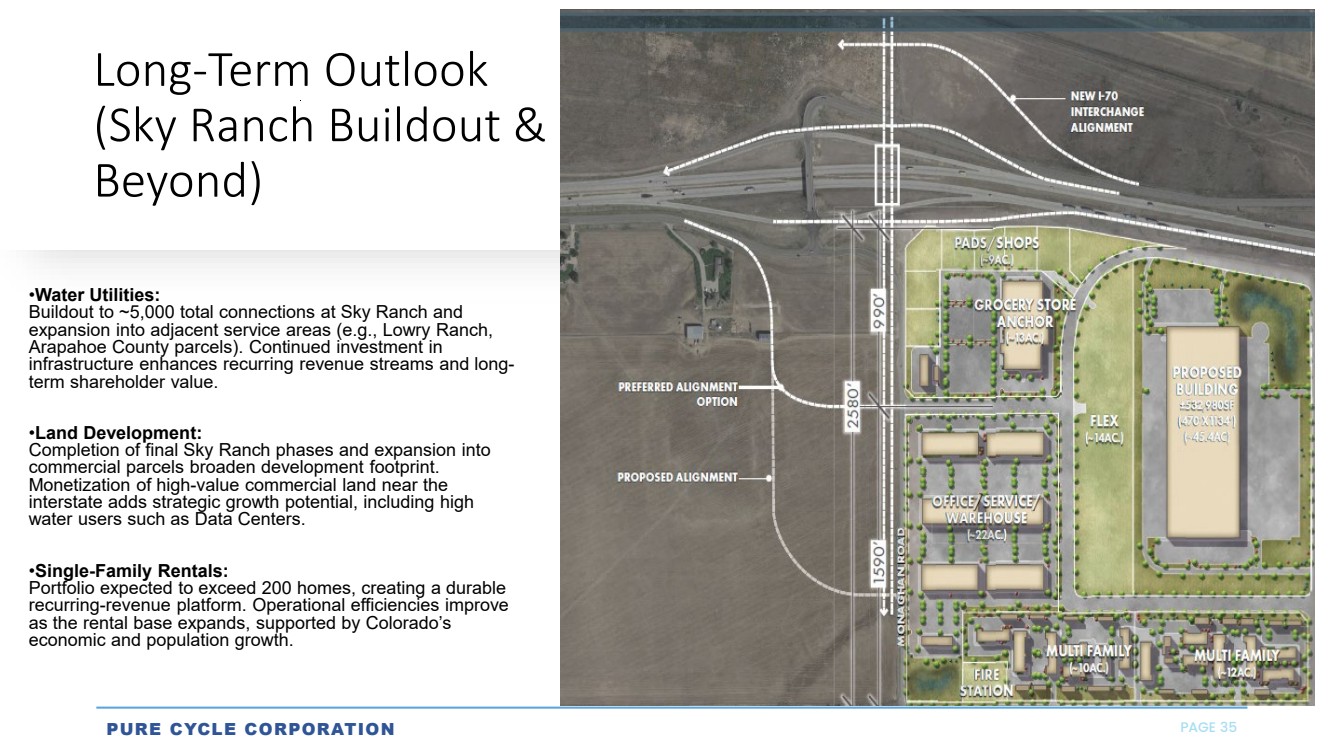

| Long -Term Outlook (Sky Ranch Buildout & Beyond) •Water Utilities: Buildout to ~5,000 total connections at Sky Ranch and expansion into adjacent service areas (e.g., Lowry Ranch, Arapahoe County parcels). Continued investment in infrastructure enhances recurring revenue streams and long - term shareholder value. •Land Development: Completion of final Sky Ranch phases and expansion into commercial parcels broaden development footprint. Monetization of high -value commercial land near the interstate adds strategic growth potential, including high water users such as Data Centers. •Single-Family Rentals: Portfolio expected to exceed 200 homes, creating a durable recurring -revenue platform. Operational efficiencies improve as the rental base expands, supported by Colorado’s economic and population growth. PURE CYCLE CORPORATION PAGE 35 |

| Earnings Presentation Q&A PURE CYCLE CORPORATION www.purecyclewater.com |